Most of us like to believe that we have a basic understanding of medical insurance terminology. The sad truth is that we really don’t. We have all heard the common insurance terms like deductible, coinsurance, copay, and out-of-pocket. We may even know the words like prior authorization or medical necessity, but dive any deeper and our heads begin to hurt. My goal is to help provide a basic understanding of how to navigate the insurance and healthcare industries. Here you will find basic insurance terms and what they really mean.

Patient Responsibility…

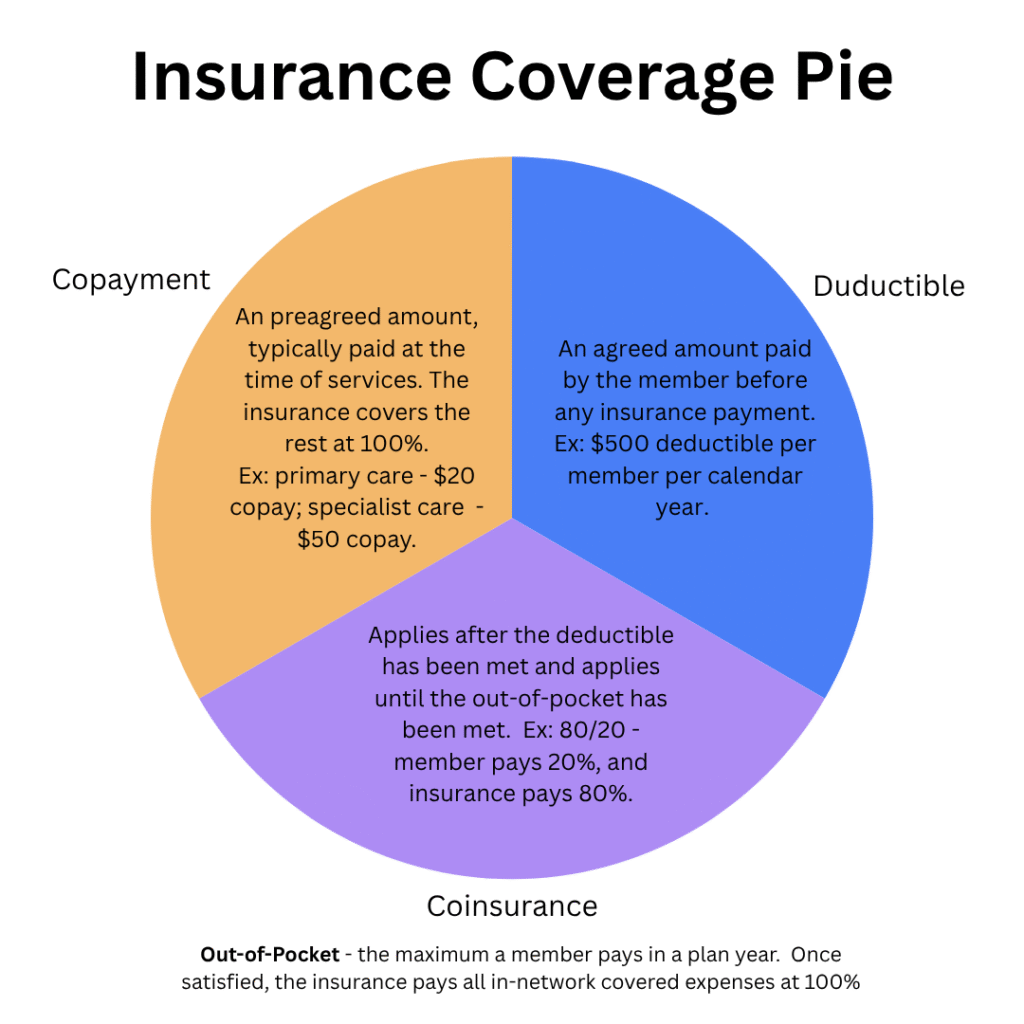

Patient responsibility (also known as member responsibility) is the bottom line of what is owed for medical services after insurance. Three main buckets make up patient responsibility: the deductible, coinsurance, and copayments. Unless the medical services received are considered preventive, there will most likely be a patient responsibility involved.

Copayments…

A copayment (copay) is a set amount paid at the time of services. Typical plans include services such as primary care, specialty care, and urgent care visits within the copay structure. Some plans include emergency care as well. Once the copay is paid, the insurance covers the remaining cost. Not all plans include copayments. The ones that do quite often have higher premiums. However, they may have lower costs when accessing care, as services covered by copays do not apply to the deductible and coinsurance. Copays do typically help to satisfy the out-of-pocket limit.

Copay plans can be tricky and a bit confusing, as most people believe that once they pay the copay, the entire visit is covered at 100%. More often than not, this is not true. In most plans, the copay covers the exam ONLY. Additional services such as X-rays, labs, or minor surgical procedures performed alongside the exam will not be covered by the copay. Instead, these services will most likely be applied to the deductible and coinsurance. Please watch the wording of your individual plan, so you are not caught off guard by a surprise bill.

For example, when our family seeks care with our primary care provider, the exam is covered with a $25 copay. However, if the provider orders tests and/ or X-rays, those services apply to our $850 deductible and 20% coinsurance. That $25 visit can quickly become quite expensive and cause a shocking bill if our family isn’t prepared for the additional patient responsibility.

Deductible…

The deductible is the portion of the bill that must be paid by the member before the insurance pays anything. As I mentioned, our family pays an $850 deductible per member per calendar year, with a cap at $2,250 for the family. This means that until I incur more than $850 worth of charges in the calendar year, the insurance will not pay anything toward my services. Once I have met the $850 or my family has met the $2,250, the insurance will begin paying toward services. It is important to note that just because the deductible has been met does not mean the insurance will pay at 100%. Many people confuse the deductible with the out-of-pocket. For most plans, the deductible is only the first part of the patient’s responsibility. This is why it is extremely important to have a good understanding of medical insurance terminology.

Coinsurance…

When thinking about coinsurance, think of cost sharing. This is the part of the plan where the patient and the insurance share the cost of services. Coinsurance does not apply until the deductible has been met. Most plans have an 80/20, 70/30, or 90/10 split. The insurance will cover the first 80, 70, or 90% of the cost, and the member pays the remaining 20, 30, or 10%. It is important to note that cost-sharing applies to the allowed charges only. The insurance may apply a provider discount to the cost before calculating coinsurance.

For example, the provider bills $300 for services rendered, but the insurance has contracted a discount for these services. The discounted amount is $200. This means that the insurance will subtract the $100 discount and apply the coinsurance amount to the remaining $200. The remaining $200 is called the “allowed amount.” This is the amount that the provider is “allowed” to charge for services based upon their agreed-upon contracted rates. With an 80/20 coinsurance, the patient’s responsibility will be $40, and the insurance will pay the remaining $160 to the provider.

Out-of-Pocket…

This is the fun part of the plan year, the part where services, even those services not considered preventive, are paid at 100% by the insurance. For most plans, this magic number is pretty high – thousands of dollars high. Our family’s plan has a family out-of-pocket of $13,500 per calendar year. This means that our family does not see 100% coverage unless we pay out $13,500 in services for the calendar year. Most plans also have an individual out-of-pocket. Anyone on the plan can meet their individual out-of-pocket and receive 100% coverage for that plan year, even if the family out-of-pocket has yet to be met.

For anyone lucky enough to meet the out-of-pocket, all in-network, covered expenses will be at no cost until the plan year ends. At which time, this amount resets to zero and needs to be met once again. To maximize the plan’s coverage, plan expensive care towards the beginning of the plan year if possible. This way, there is more time to enjoy the 100% coverage.

Diagnostic vs Preventive…

Since the dawn of the Affordable Care Act (ACA), preventive services must be covered by the insurance at 100% with no copays, coinsurance, or deductible. This is, of course, as long as the plan has not been “grandfathered.” There are a few plans still in existence that were in place before the ACA and can still have cost-sharing for preventive services. Contact your insurance to find out if your plan has been grandfathered. For our purposes here, I will only be discussing non-grandfathered plans that are mandated to provide 100% coverge for preventive services.

Doesn’t preventive mean free?

Preventive services covered by the ACA included: routine physicals, cancer screenings, chronic disease screenings, certain vaccinations, women’s health services, routine lab work, routine colonoscopies, etc. For a full list of what is covered under the ACA, visit healthcare.gov.

I won’t spend a lot of time on my soapbox preaching on the importance of preventive medicine. However, everyone with medical insurance should be taking advantage of these no-cost services each plan year. This is one way to make those premiums worth it! It’s good for your health, and your bottom line! So, don’t forget to take advantage!

It is also extremely important to fully understand your plan as it applies to preventive services to avoid nasty surprise bills. Quite a few preventive services can also be considered diagnostic. This all depends upon the circumstances that caused the services.

Colonoscopies and Mammograms…

Take, for instance, the mammogram and colonoscopy. These are both very expensive tests that providers order for two very different purposes. When done as a routine screening, these services are protected by the ACA as no-cost services. However, when done to rule out potential serious conditions, they are considered diagnostic tests and not protected under the ACA. Diagnostic tests fall under plan benefits and are subject to copays, coinsurance, and/ or deductible.

Unfortunately, insurance companies cannot know how the provider will submit the claim for these services. Insurance processes claims according to the information provided by the provider. Before having services, it is extremely important to ask the provider if they will be billing the services as preventive or diagnostic to avoid a surprise bill. I have heard of people receiving a bill of $4,000+ for a colonoscopy they thought would be free. Don’t be afraid to ask.

Advanced Written Notice or Advance Beneficiary Notice…

The No Surprises Act protects patients from surprise bills. If providers are aware that a service may not be covered, they must disclose this to patients before providing services. Because of this, many providers use what is called an “Advanced Written Notice” for commercial insurance or an “Advanced Beneficiary Notice” for Medicare. If there is a service that may not be covered by insurance/ Medicare, the provider will have patients sign this document.

These documents typically assign responsibility for services to the patient even if the insurance or Medicare explanation of benefits states otherwise. Patients have the right to refuse the services. However, if patients sign one of these forms and receive services, they are agreeing to full patient responsibility. Insurance may show a zero patient responsibility, but the provider is legally able to bill you for the full amount of services. If your provider asks you to sign one of these forms, you may want to reach out to the insurance company/ Medicare for further assistance prior to services being rendered.

Who is responsible?

Providers, employers, and insurance companies expect you to be an informed consumer of healthcare. The bill will come in your name, so it is important to understand the medical insurance terminology before seeking services. Use this post, your HR, the insurance company, and other resources to ensure you are an informed consumer of healthcare. Hopefully, this will prevent any nasty surprises and unplanned costs.